The hardest pitch in Public Relations isn’t to the media

Aobakwe Sibiya

Commenting on these, John Smyth, CEO of the bond originators Multi Net Mortgages, highlighted several salient points in the latest ABSA Home Loans Review, which he described as “always giving us a comprehensive and thorough picture of the current scene.” Almost all of the points initially selected by Smyth reflected a less than satisfactory situation, but he then went on to express a guarded confidence in the future and gave his reasons for this.

Points Smyth believes are now relevant:

“When one looks at ABSA’s latest household debt and debt servicing figures in relation to incomes,” said Smyth, “it is clear that the South African consumer is battling. Household debt now comprises about 79% of household income, a figure that is far too high for an emerging economy – and in general, debtors are defaulting more often and taking longer to pay off their loans. Although the growth in household expenditure has slowed to only 1,6%, savings have declined noticeably and it is regrettably true that almost half of South Africa’s supposedly creditworthy population are black listed as regards big loans.”

ABSA, said Smyth, have also made it clear that the amount of housing funded by mortgage repayments has continued throughout this year to deteriorate.

What, therefore, as Smyth sees them, are the encouraging factors in the current situation?

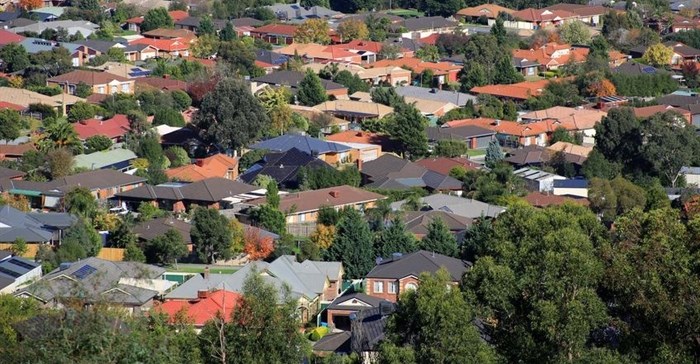

From a buyer’s viewpoint, he said, the very marked slowdown in house price growth to 4,7% this year and a projected 4,3% for 2017 will inevitably open up the market to some who right now are debarred by lack of resources. This is particularly the case in the luxury home market which flourished in 2014/2015 but is now showing close to 0% growth. Even in the popular middle segment, growth of ± 5% will before the end of this year create new opportunities for buyers.

Coupled to these facts, said Smyth, is a steadily growing appreciation among lower income earners and township residents of the value of home ownership.

“Nowhere in South Africa have house prices fared as well and resisted downturns as effectively as they have done in the former township suburbs. Here the growth is currently up to 11.90%.”

Also encouraging, said Smyth, is the surprising rise in coastal region properties, particularly those of the Cape, Southern Cape and the Hibiscus Coast (north of Durban). Here, he said, house values are growing by 8% per annum and there appears to be no end to the trend. This rise in house price growth is largely fuelled by the belief that the local government and security services in the coastal areas tend to be better than those inland.

Smyth concluded his remarks by quoting what Allister Sparks, former editor of the Rand Daily Mail and an international award winner for journalism, said at the recent Franschhoek Literary Festival.

“Mr Sparks commented that South Africa had come through so many difficult periods already that it seemed to have gained an inborn resilience and an ability to ride out extremely difficult times. There can be no doubt that current times, with the economy being in such a parlous state, are difficult – but I go along with Mr Sparks in believing that we have the backbone in the country and the housing sector to overcome all these obstacles and I predict that by the end of 2018 average house price growth across all segments will again be in a marked upward trajectory.”