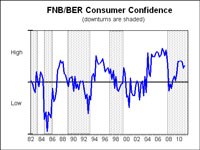

The index, just released, reveals that consumer confidence is marginally up in 2Q2011 to +11 in 2Q2011, although still lower than last year's levels, and it remained supportive of continued, if perhaps somewhat tempered, consumer spending.

The FNB/BER consumer confidence index (CCI) increased to +11 in 2Q2011 from +9 in 1Q2011.

Despite this rise, consumer confidence remained slightly below the level of about +14 registered in 2010. The current level of +11 is still relatively high given that the FNB/BER CCI averaged +6 during the previous cyclical upturn (2000-2007).

A reading of +11 indicates that a comfortable majority of consumers are satisfied with current conditions and expect these to persist over the next 12 months.

The FNB/BER CCI combines the results of three questions posed to 2 500 predominantly urban adults between 18 May and 6 June 2011, namely the expected performance of the economy, the expected financial situation of households and the rating of the appropriateness of the present time to buy durable goods, such as furniture, appliances and electronic equipment.

The questions

The reasons for the increase in the FNB/BER CCI in terms of these three questions could be summarised as follows.

Consumers became more optimistic about the prospects for the South African economy over the next 12 months compared to the previous survey. The expected economic performance index increased by 4 index points - from +13 to +17.

Consumers remained very optimistic that their own financial position would improve over the next 12 months. "This might indicate that consumers continue to expect high income growth, based mainly on increases in wages and social grants," says Cees Bruggemans, chief economist of FNB.

Although the expected household financial position index increased only marginally (from +20 to +22) in 2Q2011, the level of this index remained the highest of the three sub-indices.

The gulf between consumers' expectations about the economy and their own finances remained. Even more consumers expect an improvement in their own finances (+22) than an improvement in South Africa's economic performance (+17).

The time to buy durable goods was the only index that declined in 2Q2011. However, the decline was so small that one could argue that the index remained unchanged for all practical purposes.

A reading of -5 (-4 previously) indicates that slightly more consumers continued to rate the present time as unsuitable for buying durable goods compared to the percentage rating it as the right time.

The percentage of respondents rating it as appropriate is nevertheless higher compared to the long-term (since 1982) average of -9. It is also higher compared to the -18 registered during the recessionary second half of 2008 and the whole of 2009.

Numerous reasons why consumers remains cautious on durables

There could be numerous reasons why consumer spending on durable goods remains relatively prudent.

- Awareness of looming interest rate hikes and increased international uncertainty probably kept consumers cautious.

- The replacement cycle has started to normalise. The urgency to buy certain big-ticket items has declined because the most important ones were replaced last year. Many people, for example, upgraded their television sets before the World Cup Soccer Tournament last year. Likewise, many people have bought new cars in the last two years. Although there are probably still many people who would like to buy a car, priorities now dictate that they perhaps should postpone and make do with the old car.

- Households now find it more difficult than before the introduction of the NCA and the recession to obtain bank credit, they do not have the necessary savings and/or they do not want to increase their debt further to finance one-off big outlays.

A disconnection

In conclusion: Consumer confidence increased marginally in 2Q2011. Although marginally lower than in 2010, consumer confidence remained relatively high by historical standards.

There is a disconnection between consumers' expectations about the future and their rating of the present time. Consumers continued to remain very optimistic about the 12 month outlook for the economy and their own finances, but much less so about the present time to buy durable goods.

Consumers continued to have a high willingness to spend. However, their ability to transform this willingness to actual spending depends on the materialisation of their optimistic expectations about the future.

Should their ability to spend not improve in line with expectations (due to lower growth in real incomes and access to credit remaining limited, for instance), then the growth in actual consumer spending will ease in the near term future.

Visit the FNB Economics website at www.fnb.co.za/economics and consider using the bank's free e-mail service.

* Although the economy may already have entered an upward phase of the business cycle, the SA Reserve Bank has as yet not determined the lower turning point.

Comment: FNB/BER consumer confidence 2Q2011 robust

Cees Bruggemans (az.oc.bnf@seeC), chief economist FNB, comments:

Not every South African consumer feels or acts the same way. Nevertheless, impressive urban majorities, even with sometimes heavily skewed contributions, continue to express a comfortable, solid confidence.

FNB/BER consumer confidence rose slightly, from +9 in 1Q2011 to +11 in 2Q2011, not all that different from the +14 level prevailing throughout 2010.

This relatively high reading continues to underpin consumption intentions, provided income growth and credit access is there to sustain it. So far, into this two-year recovery it has.

Clearly, some consumer groupings are more confident than others are. Black consumers, Sotho and Nguni-speakers express overwhelming confidence.

These urban groupings show average majorities of +18 (suggesting 60/40 splits in favour of confidence), high by historic standards and more reminiscent of the late stages of expansionary upswings rather than the early phase (as the case today).

Most minorities are more coy, but mostly still helpful in sustaining the overall majority of confidence, especially when asked about their own financial prospects.

White consumers show only a small confident majority of +2, with English-speakers of all kinds (-1) and Afrikaans-speakers of all kinds (-2) not registering much different readings.

There does, though, persist a considerable gap with Black consumers (though the gap regarding own financial prospects is only one-third the size).

We can only speculate about the reasons.

Successful Black urbanites are favoured by financial and economic trends. They retain high confidence in government (going by election results) and sizeable majorities believe the economy has good prospects.

White consumers clearly have far less trust in the economy's prospects, possibly also reflecting their political views.

Yet together, along with Coloured and Indian consumers, they show comfortable majorities of confidence closely mirroring consumer-spending trends.

This is further borne out by the income categories, with all groupings retaining remarkable confident majorities, varying from +8 for low incomes (less than R2000 monthly), +10 for middle incomes (R2000-R10 000 monthly) and +16 for high incomes (over R10 000 monthly).

In each instance, own financial prospects rate even higher confident majorities, varying from +13 to +31. Historically, these are very high majorities so early into recovery.

So is there anything special going on that obviously could have a bearing on these results?

With credit access and cost severely affected by the global financial crisis and its complex aftermath and the national credit act of 2007, and the high household debt levels now for some years signalling considerable strain for many, with employment and earning opportunities severely reduced or limited, one may have expected an overwhelming lack of confidence to have prevailed.

Instead, society appears to fragment in some rather extreme factions, some highly penalised by events but others very favoured. Moreover, it is the ones enjoying benefits who seem to be the greater majorities (and presumably determining the spending outcomes).

We are talking here about those enjoying political protection and largesse (some 1.5 million public sector workers but also 15 million grant recipients), those with good talent, exceptional business acumen and/or scarce professional skills in the private sector, and those belonging to powerful unions.

At least half to two-thirds of the employable workforce appears so favoured. In contrast, those working for smaller businesses or having lesser skill or talent offerings find themselves much less benefiting in the present economic climate, with high debt levels and unemployment further overlays.

Notable tendencies in 2Q2011 were the 8 point increase in Afrikaans-speaking confidence, further mirrored by a 7 point improvement among Coloured consumers, with the Western Cape registering a 9 point improvement. In all three instances the main area of improvement was in own financial prospects.

It could be that the May local election outcome had something to do with these select gains.

The one other major structural phenomenon is the ongoing relative low confidence expressed about now being a good time to buy durable goods.

This question solicits only a -5 reading, qualitatively hugely different from answers to questions relating to economic and own financial prospects, and this across every conceivable grouping of urban consumers.

These clearly remain challenging times, with debt (and interest rate prospects) viewed with considerable scepticism.

Still, there are major differences, varying from -16 for White consumers to +5 for Black consumers, as much as -25 for English- and Afrikaans-speakers compared to +5 for Sotho- and Nguni-speakers. All forms of income differ minimally, averaging -5.

The debt question probably weighs most heavily on English- and Afrikaans-speakers, the main participants in the formal property market.

Yet overall, a -5 reading does not come close to a general recession reading. But then we are two years into economic recovery, favouring especially the motor industry but also the furniture and household appliances trades, with store-provided credit apparently plentiful.

Provided income growth in the economy continues to evolve favourable, as it has since mid-2009, with retail and motor trade credit remaining plentiful, the consumer-led revival is yet to be checked to any major degree.

This continues to be borne out by relatively high levels of consumer confidence among urban households, even if certain select groupings show much less enthusiasm than others do.

It is the overall picture that is the important one, and here we continue to see positives drivers for consumer spending, even if the actual momentum this year may be somewhat less than last year in confidence registered.

This is borne out in the motor trade, though retail sales volumes for the three months to April were still 7% up compared to a year ago, even if retailers somewhat dampened their business confidence in 2Q2011.