Top stories

More news

Marketing & Media

Thailand–South Africa Business Matching Forum brings new business opportunities to South Africa

Catalyze 3 Aug 2026

A question of timing

As we head closer to the Fed's 17 September decision on whether to raise interest rates, concerns have been growing over the decision's impact on the

global economy and emerging markets in particular. There are compelling arguments in favour of a rise - related to the domestic economy, but also as a means of ending the uncertainty that is damaging emerging markets; and equally compelling reasons to postpone - not least the timing - due to the potential impact of the flow-on effects of a China slowdown on the global economy.

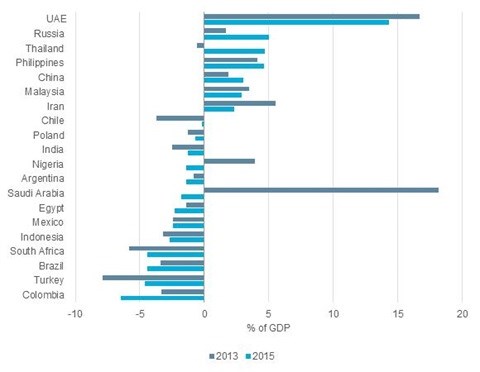

Uncertainty about the timing of the Fed rate rise continues to wreak turmoil in emerging markets, at a time when the China slowdown is impacting on commodity exporters in particular. Painting the current situation facing emerging markets as a glitch would clearly be glib, but, on the other hand, it pays to differentiate and to look at the macro-economic fundamentals. Those with weaker fundamentals - government and current account deficits, high inflation, debt burdens, over-reliance on commodities, corruption and a poor business environment are struggling most. Colombia, Turkey, Brazil and South Africa all have significant current account deficits for example, more than 4% of GDP in 2015.

Source: Euromonitor International from Eurostat/IMF/OECD.

Note: Data for 2015 are forecast.

It's a complex picture - the current account does not tell the whole story. Russia might have a current account surplus, but it has an over-reliance on oil and gas leaving it vulnerable in the face of weak commodity prices. Malaysia also has a current account surplus, but has a high government budget deficit, political instability and a certain amount of reliance on commodities.

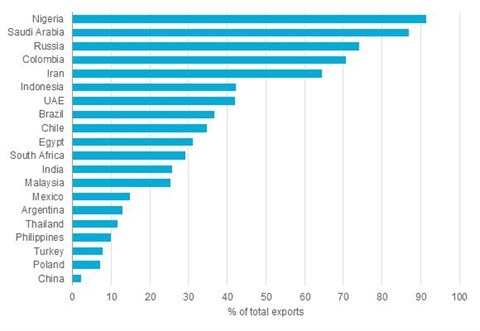

Source: Euromonitor International from United Nations (UN), International Merchandise Trade Statistics.

Note: Data refer to exports of crude materials and mineral fuels.

Whatever the immediate decision, it would be naïve to think that emerging markets can emerge unscathed in the short term; there will undoubtedly be a hangover. But it's also overly simplistic to assume all will suffer equally and that this marks the end of the ascendancy of emerging markets. Looking to 2030, emerging and developing economies are still expected to contribute 66% of real GDP growth, account for 92% of births and be home to 87% of the world's population. The script may have changed, but in the long term the story should remain a positive one.