South Africa's imports of chicken meat continue to increase as the local market is affected by high feed costs. Meanwhile, the South African government continues to evaluate the South African Poultry Association's request for an increase in the import tariff of between 12 and 37% to 82%.

Following the devastating droughts coupled with the outbreak of highly pathogenic avian influenza (H5N8) and a listeriosis food scare, the broiler industry recovered in 2018, increasing production by 6% to a record of 983 million broilers slaughtered, according to a recently published USDA Global Agriculture Information Network (GAIN) report.

Economic worth of poultry industry

The broiler industry is South Africa’s largest individual agricultural industry boasting a gross value of about US$3 billion and contributing about 17% to the total gross value of agricultural products. Commercial broiler meat production accounts for approximately 90% of the chicken meat industry, with the remaining 10% comprising subsistence farming production and depleted flock. The 983 million broilers slaughtered in 2018 equalled 1,27 million tonnes of chicken meat (excluding offal). If depleted flock and subsistence farming production is added, South Africa’s total chicken meat production for 2018 is calculated at 1,41 million tonnes, a 5% increase from 2017. A 1% decrease in chicken meat production is estimated for 2019 to 1,40 million tonnes.

High feed costs – a 70% contribution to the total cost of a broiler producer – constrained consumer demand and an expected decrease in exports are putting downward pressure on producer prices. As a result, broiler producers are expected to reduce production to 970 million broilers slaughtered in 2019. In 2020, chicken meat production is projected to increase by 2% to 1,42 million tons, under the assumption of normal weather conditions.

Poultry consumption in South Africa

South Africans consume about 3,9 million tons of poultry, beef, lamb and pork meat per annum. In 2018, the South African consumer spent approximately US$15 billion on meat products (35% of total food expenditure). Poultry meat represents more than 60% of total meat consumed. For 2018, chicken meat consumption (excluding offal) is expected to be 1,88 million tons.

The demand for chicken meat (excluding offal) is anticipated to increase by only 1% in 2019 to 1,90 million tons. This is due to an estimated economic growth of less than 1% in 2019. A 2% increase in the demand for chicken meat is expected for 2020 to 1,93 million tons.

Characteristics of South Africa’s chicken meat market

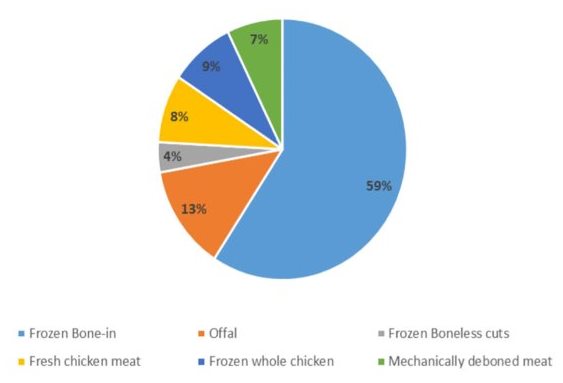

Three fundamental characteristics distinguish South Africa’s chicken meat market, which is made up of a predominantly lower-income consumer base. The first characteristic is the predominant demand for bone-in (brown meat) chicken cuts compare to breast meat. Bone-in chicken cuts represent almost 60% of total chicken meat demand mostly sold as ‘individually quick frozen’ pieces in the form of low-priced 2kg and 5kg mixed packs.

Brining is the second characteristic. Almost all locally produced frozen chicken contains brine in order to preserve and enhance the quality of the meat. In 2016, the former Department of Agriculture, Forestry and Fisheries introduced a regulation to restrict the brined content to a maximum of 15% of the mass sold. Prior to 2016, brining levels of up to 43% were recorded. The third characteristic is the relatively small demand for fresh (not frozen) chicken meat, which represents less than 10% of total consumption of chicken meat in the country.

Figure 1: The per capita consumption of meat in South Africa. Source: Department of Agriculture, Forestry and Fisheries (DAFF).

Increased reliance on poultry imports

In 2018, South Africa imported almost 520,000 tonnes of chicken meat to augment local production, up of 2% from 2017. It is estimated that this will increase by 5% in 2019 to 545,000 tonnes due to a decrease in local production on relative higher feed cost. A marginal increase in chicken meat imports in 2020 is expected (555,000 tonnes) as local production is expected to bounce back. Frozen bone-in chicken and mechanically deboned meat are the leading imported products.

Brazil is the major supplier of chicken meat to South Africa with more than 60% share in the import market. Brazil is followed by the US (16% share) and the EU (12% share).

In 2018, the International Trade Administration Commission of South Africa (ITAC) announced receipt of an application by the domestic poultry industry to increase the customs duty on frozen chicken meat imports. The application requests an exponential increase on import duties applied on boneless chicken meat and bone-in chicken meat from the current levels of 12% and 32%, respectively, to 82%, which is South Africa’s bound rate under its membership commitments to the World Trade Organisation. This issue has gained considerable attention in the media and at high levels of government. The application is in the advanced stages of the review process.

Figure 2: The percentage of chicken product consumption.

Issues with poultry export markets

South Africa’s major markets for chicken meat exports are its neighbouring countries. After the 2017 outbreak of highly pathogenic avian influenza in South Africa, many countries, including Botswana, Malawi, Mozambique, Namibia, Zambia, and Zimbabwe suspended poultry and poultry product imports from South Africa.

As a result, South Africa’s chicken meat exports dropped by more than 20% in 2018 to 51,000 tonnes. As South Africa is still struggling to reopen some closed markets and win back market share, chicken meat exports are expected to drop further in 2019 to 45,000 tonnes.

This article was originally published on Poultry World. Click here to read the original article.