Top stories

HR & Management7 reasons workers suffer mid-year blues... and what to do about it

Anja van Beek 1 day

More news

ESG & Sustainability

Africa’s sustainable fashion future to be unveiled at Twyg’s Africa Textile Talks

1 day

South Africa is a case in point. The country has an inflation target of 3% to 6% per annum, with a particular focus on the midpoint of 4.5% and keeping inflation at that level.

The point of having an inflation target is so that central banks can adjust monetary policy – in particular interest rates – with future price trends and inflation developments in mind.

Future inflation expectations determine current policy decisions. But these expectations are anchored in the credibility of past inflation figures. This aspect is often overlooked in monetary policy decisions.

The system of inflation targeting falls down if the general public doesn’t believe the historic rate of inflation. There’s been an assumption for quite some time that most people don’t believe past inflation figures. This lack of credibility was recently reconfirmed in joint research of the University of the Witwatersrand and the Professional Provident Society. The society is an insurer for professional people. It periodically does surveys among its members.

The members are professionals – including doctors, engineers, lawyers, accountants, financial advisers, academics, scientists and architects. They therefore aren’t representative of a cross-section of the South African population, but a good sample of the middle class. Nevertheless the survey results provide a good insight into the perceptions of professionals from a broad cross section of civil society.

We found that the perception of most of those surveyed was that inflation was much higher than it is in reality. This matters because the low credibility of historic inflation figures feeds into expectations about inflation.

It therefore shows that the South African Reserve Bank faces an uphill battle in anchoring expectations of future price increases at the level of the inflation target. The perception that historic price increases were higher than the target rate, feed into expectations of future price increases above the inflation target rate.

The research involved an online questionnaire to members to gauge their perceptions on a number of issues related to inflation. In total 5137 respondents provided answers.

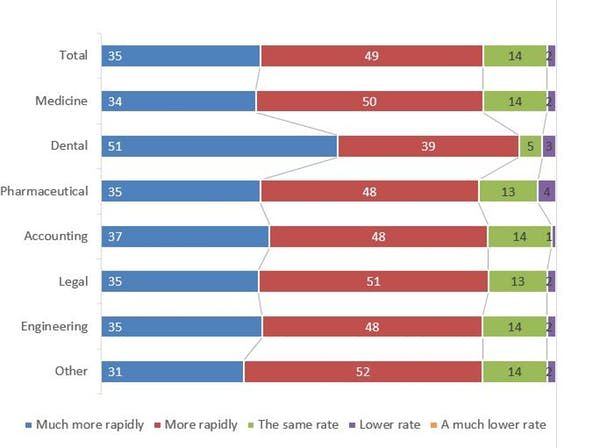

The first question put to the respondents was: over the past five years, prices in general have increased by on average 5.4% per year. During 2018, prices increased by 4,7%. In your opinion, by how much did prices increase during the past 12 months compared to the official rate?

The responses are summarised in Figure 1 below. This confirms very low credibility of historic inflation figures. On average, only 14% of respondents accepted the inflation rate as accurate, while 2% perceived inflation to be lower than the average rate. Put differently, 84% of respondents believe historic inflation was higher or much higher than reported by the official rate of inflation.

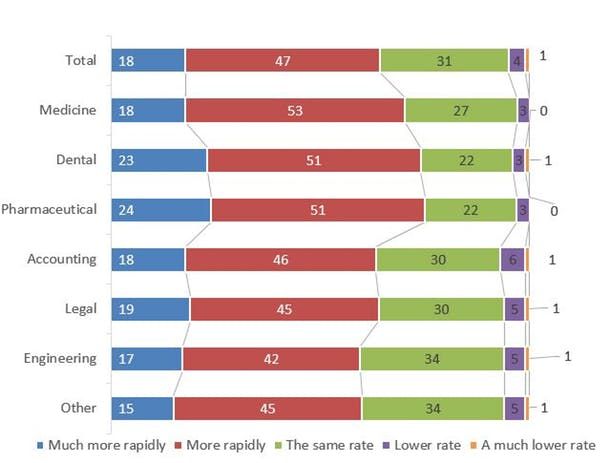

The second question put to the respondents was: compared to 2018, by how much do you expect prices in general to increase during the next 12 months?

The responses to the second question confirm high inflation expectations, these can be seen in the figure below. On average, only 36% of respondents expected inflation expectations to be anchored in the historic rate of inflation. To the contrary, 64% of respondents held inflation expectations that were much higher than the historic rate of inflation.

This leaves no doubt that the low credibility of historic inflation figures feeds into inflation expectations. People base their expectations of future inflation on their perceptions of the historic level of price increases.

The South African Reserve Bank uses the Bureau of Economic Research to measure inflation expectations. In its survey, the bureau only focuses on the inflation expectations of respondents and not on their perceptions of past inflation. The survey should be expanded with a question perceptions of historic inflation, thus expanding the focus of the sample to both inflation perceptions and inflation expectations.

In their quest to contain future inflation expectations, central banks should address the problem of a lack of credibility in historic inflation figures. Inflation expectations will only be anchored in current inflation rate once the credibility of current inflation figures is established.

Owing to a lack of credibility in the historic inflation figures, there is an upward bias in inflation expectations that needs stricter monetary policy and higher interest rates than would be the case with credible historic inflation figures. Until there is general acceptance of the accuracy of historic inflation figures, it will be necessary for the central bank to err on the side of caution in setting the level of future interest rates.

This research on inflation perceptions shed some light on the formation of inflation expectations, which is missing from South African research. In South African research on inflation expectations, respondents are not asked questions on aspects informing their level of inflation expectations. Likewise, the society’s survey does not ask for specific indicators of reasons why respondents perceive historic inflation above the official rate of inflation, it merely asks for an overall perception. These are areas for future research.

This article is republished from The Conversation under a Creative Commons license. Read the original article.![]()

The Conversation Africa is an independent source of news and views from the academic and research community. Its aim is to promote better understanding of current affairs and complex issues, and allow for a better quality of public discourse and conversation.

Go to: https://theconversation.com/africa