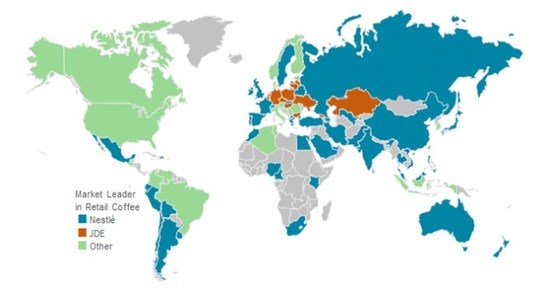

Jacobs Douwe Egberts (JDE) and global market leader Nestlé are in a market struggle, since the formation of JDE in 2015. JDE holds the leading position in coffee in a band stretching from Belgium through Central and Eastern Europe and the former Soviet Union, while Nestlé has the edge in the western edge of Europe, Australasia and much of Asia, the Middle East, Africa and Latin America.

Other major coffee companies may harbour ambitions of one day becoming truly global players, but right now, no one else is even close to matching their geographical reach.

Outside of North America, market leader in most countries is either Nestle or JDE

Growth in JDE’s core Central and Eastern European markets, though, is going to become increasingly hard to come by. That means that if JDE is serious about gaining share on Nestlé globally, it will have to shift a significant amount of its focus to the developing regions that are the drivers of global coffee growth.

To do this, JDE only has a few geographic options going forwards. One is Latin America, but outside of Brazil, the company has no meaningful presence and Nestlé is firmly entrenched at the top of key markets like Mexico. Another is the Middle East and Africa, but JDE is actually losing share in the Middle East now, hardly an encouraging sign. That leaves Asia, more specifically, Southeast Asia. Rapidly expanding markets, a favourable competitive landscape and the recent purchase of Singapore-based Super Group all make this the key area where JDE needs to succeed if it is to make a challenge to Nestlé’s global coffee leadership.

Source: Euromonitor International

Europe-driven strategy not an option

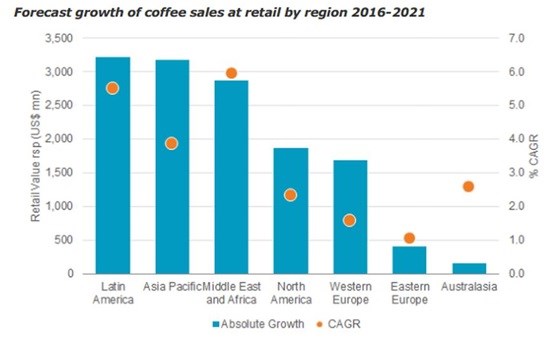

Western European coffee will grow by $1.7 billion during the forecast period and Eastern Europe will add another $398 million. However, JDE is unlikely to gain much globally on Nestlé by relying on Europe. The recent forced sales of Carte Noire and Merrild for antitrust reasons have shrunk the company’s European sales considerably and made it so that JDE will be forced to rely on organic growth in Europe for the near future.

While there is certainly organic growth to be had, it is nearly entirely restricted to fresh ground pods. JDE is well positioned to benefit from that, but it is also heavily exposed to the contracting instant and standard fresh ground categories, meaning that overall European growth will be weighed down heavily no matter how many more pods JDE is able to sell.

Nestlé, more exposed to the declining instant category because of the omnipresence of Nescafé, will probably take a heavier hit in Europe, but Nespresso and Dolce Gusto should keep sales positive. This means that while JDE will probably outgrow Nestlé in Europe in the near future, it is unlikely to be enough to make up significant ground globally.

Challenges of Latin America, Middle East

Of all the developing regions, JDE is by far the best established in Latin America, where it generated over $900 million in sales in 2016. Its geographical presence in coffee, however, is restricted to just Brazil. In the rest of the region, JDE is absent, while Nestlé has an immensely strong position, with over half the market in important countries such as Mexico and Chile.

While in theory, JDE could try to muscle in, it would likely prove tough going. Nestlé is holding or gaining share in all the key markets through more premium brands such as Nespresso and Taster’s Choice. Acquisition of a local brand is always an option, but there are few brands successfully beating Nestlé now. There is the option to try to generate more organic growth out of the large Brazilian market but Nespresso is surging here too and JDE is struggling to hold onto the share it has, let alone gain more.

The Middle East and Africa is also an area of major forecast growth, but one with its own set of challenges for JDE. It is moving in the wrong direction in the region and slipped to third place in 2016 behind Lavazza, with a growing Tchibo moving within striking distance. The issue here is the Middle East, where JDE share peaks at 6% of the Israeli market, falling to 1% in Saudi Arabia and none at all in Egypt or Iran.

Nestlé is hardly untouchable in the area (Lavazza gained seven points of share in Iran during the review period), but JDE has proven unable to capitalise on that and has made no major moves in the area since being formed. The situation is better in Africa, where JDE is a significant player in Morocco and South Africa, but being largely shut out of the high-growth areas of the Middle East is a serious problem and one that will be difficult to reverse.

Source: Euromonitor International

Southeast Asia will prove decisive

On the face of it, Asia is JDE’s weakest developing region, where it ranks ninth by share. However, in October 2016 JDE announced it was spending over US $1 billion to acquire Singapore-based Super Group, a move that instantly boosts JDE’s Asian sales by 44%.

Significantly, Super Group gets its sales entirely from Southeast Asia, which is expected to see the most dramatic coffee growth of anywhere in the world. No less than four of the top 10 growth markets in coffee globally are located in Southeast Asia. Nestlé is also much more vulnerable here than elsewhere and is struggling to fend off local companies like Kapal Api Group in Indonesia and JG Summit Holdings in the Philippines. This somewhat confused competitive landscape presents an opportunity for JDE.

There are many Super-like brands growing strongly that are not attached to a big international player, which may be open to purchase or partnership agreements. This could provide a way into the booming markets where JDE currently has no presence, including Indonesia, the Philippines and Vietnam. JDE’s absence from these countries is a serious weakness and one that it should be a major priority to rectify. Those three will combine for nearly US $2 billion in absolute growth during the forecast period, some four times more than the rest of Southeast Asia combined.

Many local companies play heavily on the fact that they are producing their coffee locally, especially in Indonesia, so if JDE does purchase one of these local companies it will have to take care to ensure that it still feels like a local brand. Also of note is that the driver of growth here will be instant coffee mixes, which is true nowhere else in the world, so new product development will have to prioritise creating mixes that appeal to local tastes rather than adapting products that have been successful in other regions.

Europe coffee market declining

In 2011, Europe (East and West combined) represented 42% of the global coffee market, but by 2021, it will be just 33%. With Europe decreasing in importance globally with each passing year, a Europe-first coffee strategy is not tenable if JDE hopes to compete with the globally diversified Nestlé. Increasing its presence in the boom markets of Southeast Asia is not the only route through which this could happen, but it is the most promising one.

A JDE, with major share in Asia, would be a company that could put considerable distance between itself and its European-focused rivals such as Lavazza, Tchibo and Strauss. That would leave only Nestlé as a major challenger and leave the two to battle it out on a global scale for the emerging coffee powerhouses of Africa, Asia and the Middle East.