According to the latest Construction Industry Development Board (CIDB) Business Conditions Survey, overall conditions in the South African construction sector in the third quarter of this year were little changed from those in Q2.

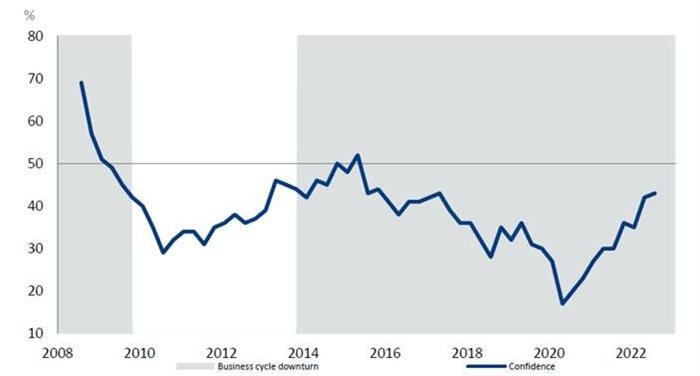

The SME Business Conditions Index moved from 42% to 43%, reflecting an improvement in activity, while both confidence and activity were above the long-term average, with order books looking healthier. Demand for new work increased while profits were better. The constraint of insufficient demand improved significantly and is now below its long-term average.

Sentiment improved for both general building (GB) and civil engineering (CE) contractors. Skilled labour and building material constraints eased, however, access to credit became more difficult. Rising interest rates might be affecting building contractors.

These findings are the quarterly results of the SME Business Conditions Survey conducted by the Bureau for Economic Research (BER) on behalf of the CIDB.

“Recovery in the construction sector continues, albeit at a slow pace,” says Bongani Dladla, CEO of the CIDB.

"The sector was grievously mutilated by the economic slowdown in South Africa, hit again by the Covid-19 pandemic, and is suffering from the uncertainty brought on by load shedding.

“There is no doubt that the third quarter has seen a continued strengthening of the sector as a whole and is a hopeful indicator that better days lie ahead.”

Figure 1: CIDB SME Business Conditions Index. Source: BER

The BER survey polls senior executives in the building and civil construction sector in Grades 3 to 8. Survey results varied across the overall sector.

General building sector

In the general building sector, more than half of the respondents were still dissatisfied by the present business conditions, although the level of dissatisfaction is much better than the long-term average. Thus, confidence ticked up by two points to 46%.

Activity was better and is now just above the historic average, yet lower than a year ago, with a continuing shortage of skilled labour. Tendering competition declined to an all-time low – possibly due to more projects going out to tender or fewer contractors tendering for projects.

A good indicator was that profitability is at its highest since 2018.

Civil engineering sector

In the civil engineering sector, confidence continued to rise, reaching a joint highest level in the last four-and-a-half years. This was supported by a significant increase in activity, plus employment and profitability at their best levels since the start of 2021.

Business conditions improved in the third quarter, but expected business conditions worsened, yet are still in line with those since the beginning of last year. Surveyed constraints eased, inclduing insufficient demand, and shortage of skilled labour and supply of building materials: the latter despite supply disruptions, which have improved.

Inadequate access to credit declined, nonetheless, it remains slightly above the historic average. “The civil engineering sector appears to have taken a positive step forward and it is a good omen for the future,” says Dladla.

Confidence across grades

The contractors in the different grades experienced varying outcomes. Confidence in CIDB Grades 3 and 4, as well as 7 and 8, were well above their historic averages while Grades 5 and 6 fared worse.

For Grades 3 and 4, activity improved. The constraint of insufficient demand eased, while employment and profitability increased. For Grades 7 and 8, a notable improvement in activity and profitability was behind the leap in confidence. Sentiment was at its highest since 2016. The same is true for profitability, albeit coming off a very low base.

For Grades 5 and 6, the picture was different. Confidence declined as activity improved, even so, business conditions worsened, profitability deteriorated while tendering competition was keener, and access to credit more difficult.

Confidence in major provinces

As with the grades, so with the provinces. In the Eastern and Western Cape, confidence fell, while it remained unchanged in KwaZulu-Natal (KZN), and it soared in Gauteng. In the first two first cases, this was despite an increase in activity, while in KZN, the opposite held, and yet confidence remained steady. Insufficient demand eased, possibly indicating healthier order books.

In Gauteng, there was a significant improvement in activity, although off a very low base and merely a recovery from the second quarter this year. Insufficient demand decreased, tendering competition was higher than elsewhere in the country - thus, it is possible that larger contractors are driving activity in Gauteng.

Says Dladla: “The overall picture for the construction sector is improving, but there is still a long way to go.”