Given the rapid rate of change in the last 18 months, what has become increasingly evident is that a number of long-held assumptions about consumer behaviour is no longer true. Target Group Index (TGI) data reveals that income and particularly disposable income levels have shifted significantly as consumers spend and even think about money differently.

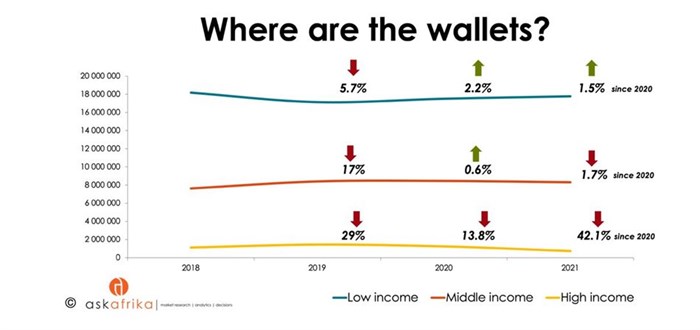

According to founder and CEO of Ask Afrika, Andrea Rademeyer, the pandemic has had profound implications for disposable income with the number of high income earners dropping 42.1% during the pandemic.

“High income individuals are no longer the core market,” she reveals. “Instead they represent just 3% of the market and are showing a decline. This means it particularly important for marketers to understand and define the remaining 97% of the market. Getting this right requires segmenting and defining your brand’s positioning or product differentiation for each segment and understanding your current penetration and opportunity.”

TGI data reveals that both more affluent and less affluent groups include segments who are taking strain financially and living from pay check to pay check. Living month to month, therefore, is not exclusively the result of income levels but has more to do with how well individuals are managing their expenses and their lifestyles, which in turn is being driven by their attitudes towards finances, including budgeting, saving, debt and insurance.

Similarly, there are individuals from both affluent and less affluent groups who believe they are managing financially, which in most instances, again relates back to how they think about money.

“Financial behaviour and mindsets are similar across income brackets. As a result, marketers need to be careful not to stereotype as this could potentially alienate your market. Instead, understand behavioural economics and psychographic behaviour to better understand how your market thinks and acts.”

What this indicates, says Rademeyer, is that marketing strategists may be better served looking for similarities as opposed to differences between different groups of people. “Our obsession with race and gender seems to be less relevant in a more integrated economy and consumer base,” she says. “The assumptions about upper and lower income groups having very different financial values has been proven to be incorrect, in the same way that the assumption that the poor are price-obsessed has repeatedly been proven to be wrong by our research over the last few years. In fact, our research indicates that value and reliability matter far more to those with a restricted income than price.”

These are not the only traditional assumptions that are being over-turned. Contrary to the assumption that lower income markets use mass and traditional media, TGI data indicates that all income groups are utilising online shopping. However, key to growing e-commerce in less affluent areas is for data costs to be reduced.

“Digital natives are everywhere,” says Rademeyer. “Ultimately, marketers need to understand which media their customers are consuming and then form an uninterrupted and consistent conversation with these consumers, differentiating themselves with the content they use.”

TGI data reveals that brand loyalty is at its lowest level since 2003, having dropped 8% during the Covid-19 pandemic, as speed and convenience trump loyalty and even price. As brand loyalty declines, marketers need to be more precise than ever in understanding their consumers – which is where credible, data-based intelligence needs to come in.

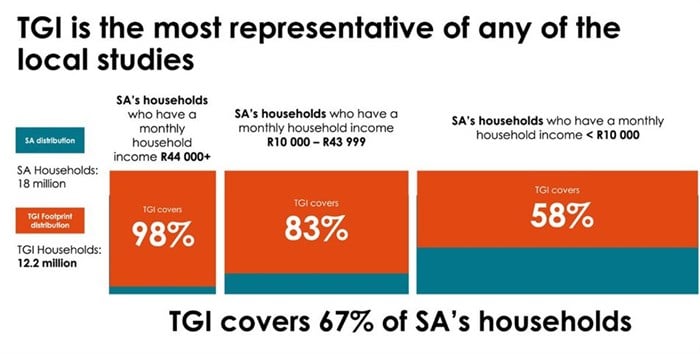

Although there is an assumption that TGI is a middle class survey, Rademeyer reveals that an in-depth analysis of the study’s sample and income indicators reveals that it is the most representative upper income survey available which is why Ask Afrika is able to so confidently predict new consumer segments.

What TGI’s results reiterate, says Rademeyer, is the fact that South Africa is a unique country and needs to be understood from a local perspective. Marketers focusing on South African consumers need to be focusing on mindsets and lifestyles within each income level in order to genuinely understand and engage with their markets.

For more information, please contact Maria Petousis on az.oc.akirfaksa@sisuotep.airam or Simone Kakana on az.oc.akirfaksa@enomis

Web portal: www.askafrika.co.za | + 27 (0) 12 428 7400 | az.oc.akirfaksa@tcennoc