Coface, the international credit insurer, has released its latest research on Brazil. Coface looks at the root causes of the recent demonstrations in a country that will host the World Cup in 2014 and the Olympics in 2016.

Demonstrators' demands are both qualitative and quantitative in nature. They concern political practice, education, health, transport and housing. Though the president says she is determined to respond to the demands, the responses made will inevitably take time.

Ranked seventh in the world (and the second largest emerging economy) by GDP size, Brazil is the archetypal emerging country. It brilliantly passed the test of the 2009 economic crisis, demonstrating the strength of its economic fundamentals and the maturity of its political institutions.

However, the Brazilians' legendary optimism has been sorely tested in the last two years: weak growth, loss of industrial competitiveness and, more recently massive protests. Can the Brazilian economy be repaired?

Challenges to repairing the economy

The weak growth and the social tensions are the result of structural problems relating less to classical economic policies than to reforms affecting the country's infrastructure and education; matters which, as Cristiano Souza of Santander emphasises, "cannot be resolved in the short term".

According to Luiz Rabi of Serasa, low growth means there will be no decline in the company bankruptcy rate. On the one hand, businesses are benefitting from healthy household demand, but on the other hand, interest rates and the weakness of global activity are affecting performance.

In all sector analyses (chemicals, steel, automotive, retail and agro-food) the notorious "Brazil cost" comes up again and again as a decisive disadvantage. For example, the cost of energy is a burden on the steel industry and upward pressures on wages are eroding the competitiveness of the chemical industry.

Small producers in the agro-food sector suffer from a lack of access to new technology. However, Brazil's entrepreneurial fabric benefits from two key strengths.

First, the heavy involvement of the authorities is a constant - even to the extent of adopting protectionist measures.

Secondly, the growth in middle class incomes is contributing to the rise in prices, but is sustaining the automotive industry and retail trade, two key sectors. The Brazilian middle class is attracting profit-seeking international investors, as evidenced by the interest of Korean and Chinese car manufacturers. In short, the country holds all the cards needed to inspire the hope that this immense market will take off again.

Dampers on Brazilian optimism

Growth figures continue to put a damper on the legendary optimism of the Brazilian people. In 2012, economic activity was the weakest registered among the BRICS countries at 0,9% compared to an average of 4,8% for all emerging countries. Q1 2013 was again disappointing, especially as a clear upturn was expected. Activity grew by a meager 1,9% over one year.

These disappointing growth numbers were exacerbated by persistent inflation with consumer prices rising by another 6,5% in May 2013. This quasi stagflation is one of the reasons - among others - behind the widespread social unrest that has taken hold since mid-June 2013.

Stagflation brings with it a dilemma for monetary policy - whether to encourage the recovery and accordingly lower interest rates, or to do the opposite and increase interest rates. Finally, Brazilian stagflation is affected by structural factors - the notorious "Brazil cost" - which has become an economic issue: labour market tensions, loss of competitiveness and infrastructure shortcomings, all reasons for Brazil's economic woes.

Stagflation - a worrying cocktail

Contrary to the legend and especially regarding other emerging countries, Brazil is characterised by potentially limited growth. GDP grew by an average 3,6% between 2000 and 2011, far behind China (10,2%) and Russia (5,3%).

This comparatively modest growth rate is explained by structural factors typical of Latin America, namely a low rate of investment compared with Asian economies (18% of GDP against 45% on China). Brazil's growth is volatile, as dynamic internal demand tends to aggravate the current account deficit, which then sharply readjusts itself.

Chart 1 - GDP

In short, Brazil is accustomed to booms and busts, as shown in Chart 1, which links the GDP growth rate with the current account balance since the 1980s. As we can see, following a record boom in 2010 with growth touching 8% which looked like a clear overheating of the economy, 2011 and 2012 were, as expected, years of more subdued activity. In essence, a typically Brazilian cyclical component explains the observed slowdown.

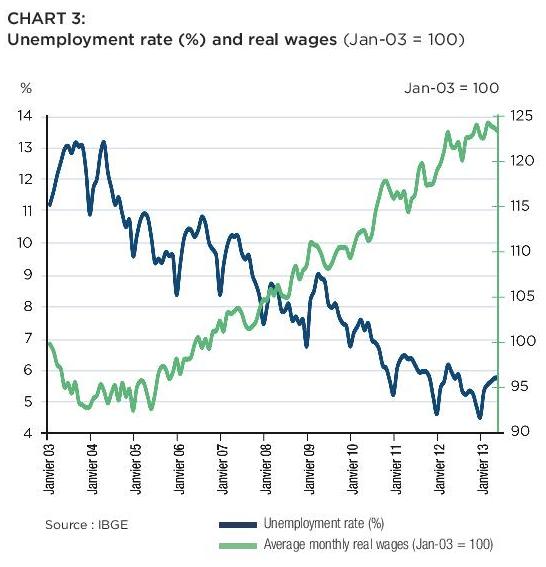

The labour market is tight

Brazil's unemployment rate has fallen sharply since the early 2000s, dropping from 12,4% in 2003 to only 5,5% in 2012, and stabilising at 5,8% in May 2013. While it is true that this situation of near full employment buoys household consumption, it could push up wages and add to inflationary pressures and at the same time put company profits under pressure.

On top of this, the minimum wage was again increased by 9% on 1 January 2013, and unemployment continues to be below the so-called natural unemployment rate - i.e. at a level compatible with low inflation estimated at about 6%.

Tensions in the labour market do not seem to be easing, despite the context of weaker growth that has characterised the country since mid-2011. Productivity is also still disappointing, due notably to the lack of a qualified workforce and the preponderance of underperforming service sector jobs which accordingly contribute little to the country's growth.

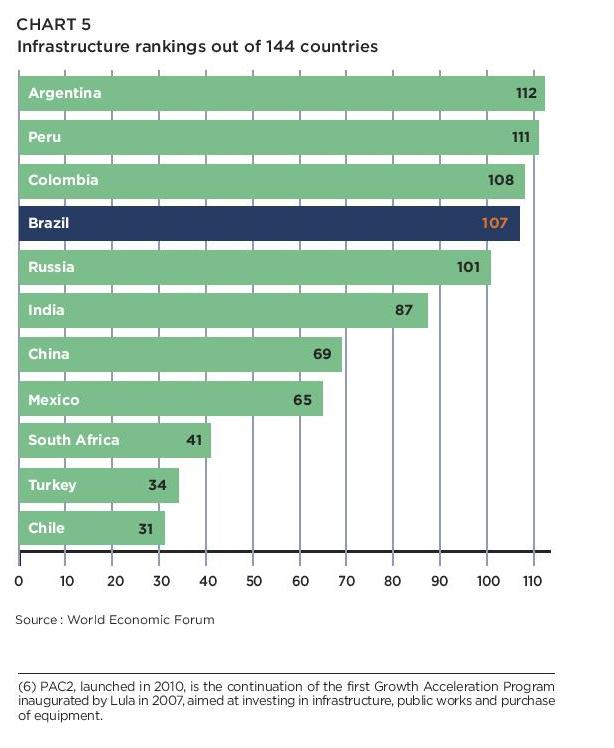

Chart 2 - Infrastructure rating

Infrastructures are deficient

The cost of labour is not the only obstacle to Brazilian growth. According to the last BRICS figures regarding infrastructures, Brazil is struggling to improve its infrastructure despite the many projects in the run up to the Football World Cup in 2014 and the Olympic Games in 2016.

This is due to the poor quality of roads, port, air and rail infrastructures. The authorities are, however, committed to increasing expenditure and are trying to encourage large-scale infrastructure investment, linked especially to the two major sporting events on the horizon.

In 2012, President Dilma Rousseff unveiled a massive stimulus package based on public/private partnerships and the opening up of road, rail and airport concessions. Investors are still hesitant in the face of burdensome bureaucracy, administrative red tape and excessive and ineffective taxation, exacerbated by a desire for greater State control over the economy.

There are, therefore, persistent doubts as to the country's internal capacity to implement the investment projects announced, especially as major investment projects have to date not progressed at the desired rate, as shown by delays in the major projects launched by former president Lula or progress on the Growth Acceleration Program (PAC2) on which only 30% of the planned budget was disbursed in 2012. These chronic infrastructure shortcomings continue to substantially impede the country's growth.

Chart 3 - unemployment rate

The cure for Brazil's stagflation lies, not in economic policy, but in reforms to improve education and thereby increase the number of qualified workers. There must be a drive to improve infrastructures if the country is to avoid bottlenecks. However, this is difficult medicine to take and the results will only become apparent in the long term. In the meantime, the population is becoming impatient.

For more information, go to www.cofaceza.com.

{kind=link}

{kind=link}

{kind=link}