According to statistics from the Q3 2021 Oobarometer, despite the ongoing upheaval caused by the Covid-19 pandemic, coupled with civil unrest in KwaZulu-Natal and Gauteng, lending conditions remain advantageous to home loan applicants.

Says Rhys Dyer, CEO of ooba: “The pandemic has drastically changed consumer behaviour as well as banking trends, resulting in a surprising boom in the local residential property market over the past 12 months. Continued competition amongst the major banks for a bigger share in the home loans market has translated into higher approval rates as well as offers of attractive interest rates below prime. Added to the mix, local interest rates remain at their lowest level in 50 years.”

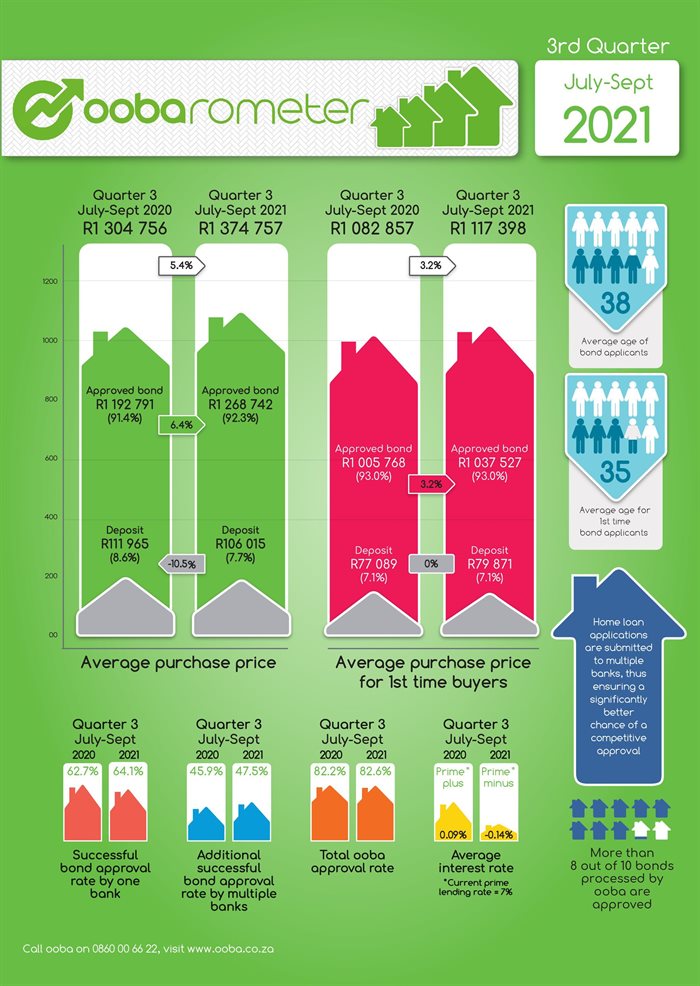

“These factors combined suggest that home buying and mortgage lending have to date remained relatively immune to the pandemic. Despite slower growth in property prices for this quarter, we expect growth in residential property prices to continue,” says Dyer. The Oobarometer statistics show a retreat this quarter from previous double-digit to single-digit property price growth with the average purchase price increasing by 5.4% year-on-year compared to the third quarter of 2020 (Q3 20).

Fiercely competitive lending landscape

Rhys Dyer, CEO of Ooba

Dyer adds: “The local banking industry also appears to be optimistic about the future of the South African residential property market. The current lending landscape remains fiercely competitive, which is evidenced in the softening of their deposit requirements and their approvals at interest rates on average below prime.” Ooba’s stats for Q3 21 shows that the average deposit as a percentage of the purchase price declined by 10.5% year-on-year. Ooba secured an average interest rate of 0.14% below prime in Q3 21 for its successful home loan applicants, 23 basis points cheaper than Q3 20’s prime plus 0.09%.

Of all home loan applications received by Ooba in Q3 21, 50% were from first-time homebuyers. Almost 63% of Ooba’s first-time buyer applications in Q3 21 were for zero-deposit bonds compared to 60% in Q3 20.

Says Dyer: “Zero-deposit bonds are very sought after amongst first-time homebuyers. Our approval rate for 100% bond applications this quarter was 81.5%, up by 1.4% on the third quarter of 2020. The willingness of banks to offer low or no deposit loans creates the ideal environment for new entrants to the property market.”

With the lower cost of borrowing boosting affordability, Ooba’s statistics show growth in homebuyers buying alone as opposed to co-buying, to become the exclusive owners of their property. This segment of homebuyers has grown to close to 60% of Ooba’s applications processed since the beginning of the pandemic.

Women dominate single-owner segment

Female homebuyers currently dominate this single-owner segment, constituting over 51% of applications received by Ooba. Since April 2020, applications from women buying on their own increased by 4%.

Dyer adds: “Purchasers buying properties as buy-to-let investments increased to 7% of applications received by Ooba in the third quarter, compared to 5% in the third quarter of 2020. Current lending and buying conditions are perfect for property investors.”

Banks’ decisions on credit and pricing can vastly differ, as indicated by the record-high ratio of 47.5% of applications that are initially declined by one bank, but approved by another bank in the Oobarometer statistics.