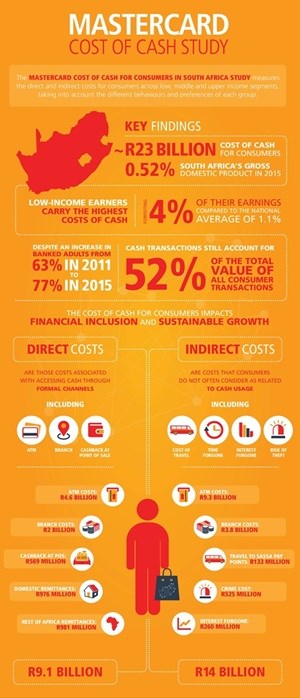

Despite an increase in the number of banked adults from 63% in 2011 to 77% in 2015, cash transactions still account for more than 50% of the total value of all consumer transactions. This suggests that being formally banked may not be enough of a driver for consumers to move away from cash.

“Adoption of products is an important first step for financial inclusion but usage is equally important,” says Mark Elliott, division president of Mastercard, Southern Africa. “From the consumer’s perspective, the perceived benefit of using cash is largely driven by the misconception that cash is cheap. While South Africans are generally aware of the direct fees associated with accessing cash such as bank transaction fees, they do not consider the indirect costs such as travelling to cash-in and cash-out points, the often billable time lost spent accessing cash, as well as the risk of theft.”

Conducted by Genesis Analytics, the study measures both the direct costs of cash (ATM, branch costs and cash-back at point of sale) and indirect costs of cash (travel costs, time-related costs, foregone interest and theft) for consumers across low, middle and upper-income segments, taking into account the different behaviours and preferences of each group.

Invisible costs of cash

The study found that the indirect cost of using cash accounted for 61% of the total cost of cash to consumers, with low-income earners carrying a heavier burden than middle- to high-income earners. This is largely driven by the higher indirect costs, including travel time, travel costs and low access to alternative channels, such as internet banking, which is generally cheaper than traditional ATM and branch withdrawals.

“Cash is the enemy of financial inclusion and of the poor. Too many South Africans still need to trade off the demands of an hourly job with the need to travel long distances to access cash or stand in line to pay a bill. Many consumers also face the dangers of being robbed when they come home with their wages,” says Elliott.

The study further reveals that low-income earners – 46% of whom are banked – tend to use cash because of very limited card acceptance at micro-merchants, particularly in rural and peri-urban communities where there is no alternative to cash.

This slow adoption of alternative channels is also evident in remittance payments. The cost to remit cash both locally and to the rest of Africa accounted for 8% of the total cost of cash to the consumer, with the bulk of the cost comprising informal remittance channels, which are most dominant in remittance flows to the rest of Africa.

Elliot concludes, “If we are to accelerate the migration of South African consumers to a cashless and financially inclusive society, the payments industry must focus on:

• improving accessibility to alternative payment channels

• educating consumers and merchants on the true costs and danger of cash

• looking at behavioural interventions such as offering immediate and tangible rewards for using a card to change people’s bad habits”