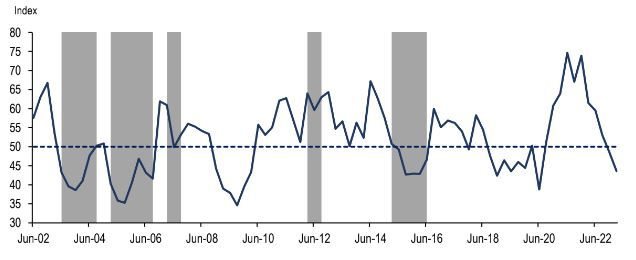

After a 4-point decline in Q4 2022, the Agbiz/IDC Agribusiness Confidence Index (ACI) deteriorated further by 5 points in Q1 2023 to 44. The current reading is the lowest since Q2 2020 when Covid-19 lockdown restrictions were first implemented. Notably, the first quarter reading is below the neutral 50-point level, implying that agribusinesses are downbeat about business conditions.

Source: ©joruba via

123RFThe persistent and intense episodes of load-shedding, higher input costs, rising protection in some export markets, rising interest rates, intensified geopolitical tensions which disrupted supply chains, and ongoing weaknesses in municipal service delivery, and network industries were again the key factors survey respondents cited as their primary concerns. This survey was conducted in the final two weeks of February, covering businesses operating in all agricultural subsectors across South Africa.

Figure 1: Agbiz/IDC Agribusiness Confidence Index

Source: Agbiz Research, South African Weather Service(Shaded areas indicate periods when rainfall across South Africa was below the average level of 500 millimetres)

Discussion of the subindices

The ACI comprises ten subindices, and six declined in Q1 2023. This excludes the debtor provision for bad debt and financing costs subindices, which are interpreted differently from other subindices. Here is the detailed view of the subindices.

• The turnover subindex fell 9 points from Q4 2022 to 69 points. Nevertheless, this current level is well above the long-term average, signalling that many farmers continue to benefit from relatively high crop prices, specifically grains and oilseeds. Moreover, the expected large summer crop harvest in the 2022/23 production season also provides support.

• The market share of the agribusiness subindex dropped by 10 points in Q1 2023 to 58. The respondents that mainly drove this notable decline are within the horticulture and livestock subsectors.

• The employment subindex declined by 12 points from Q4 2022 to 47. This is below the 50 neutral point and signals concerns about employment conditions in the sector. There was a downbeat sentiment among most respondents. In Q4 2022, there were about 860 000 people employed in primary agriculture, down 1% q/q and y/y.

• The capital investments subindex fell 7 points from Q4 2022 to 59. This is unsurprising as the rising interest rates and frequent load-shedding continue to weigh on businesses.

• The general economic conditions subindex fell by 14 points to 11 in Q1 2023. This is the lowest level since the second quarter of 2020, when Covid-19 lockdowns were first implemented with various sectors closed, except for agriculture and the food value chain. The bleak assessment of general economic conditions speaks to the current challenging business conditions brought by persistent energy shortages, inefficiencies in the network industries, inflation concerns, and rising interest rates, amongst other challenges.

• The general agricultural conditions subindex fell 9 points to 31, the lowest level since Q4 2019. This perhaps reflects the effects of excessive rains at the start of South Africa's 2022/23 summer crop production season, which created challenges for farmers and agricultural role players. Crop planting in various regions of the country was delayed by roughly a month, threatening yield prospects. But the warm weather at the end of January and much of February helped improve conditions on the farms.

It thus eased concerns about the possibility of smaller yields due to excessive soil moisture. Moreover, the persistent load-shedding raised concerns that areas under irrigation could receive poor yields. Still, the return of rainfall, at a moderate pace, from mid-February provided a much needed breather and improved crop conditions.

• Unlike the rest of the subindices, the net operating income subindex was up by 2 points to 61, mainly reflecting better operating conditions in the grains and oilseeds businesses.

• The sub-index measuring the volume of exports sentiment lifted by 13 points from Q4 2022 to 63. This is unsurprising given the solid export activity we observed in 2022, and there are hopes that it will continue this year, notwithstanding worries about crop conditions in some areas. South African agricultural exports were up for the third consecutive year in 2022, reaching US$12.8 billion, up 4% from the previous year.

• The subindices of the debtor provision for bad debt and financing costs are interpreted differently from the abovementioned indices. A decline is viewed as a favourable development, while an uptick signals growing financial strain. In Q1 2023, the debtor provision for bad debt was up by 2 points to 36, which is unfavourable and signals growing worries about financial conditions in the sector.

Meanwhile, the financing costs indices surprisingly fell marginally by one point to 3. This marginal change confirms that there are still concerns about relatively higher interest rates.

The Agbiz/IDC ACI's Q1 results show growing concerns amongst the agriculture and agribusiness role players about the economic conditions of this sector. Addressing the electricity crisis, and sector-focused issues such as biosecurity, opening up more export markets and dealing with inefficiencies in municipality service delivery are some of the key issues that will help improve sentiment and the fortunes of our agriculture and agribusiness sectors.