2017 was not the greatest year for South Africa and while the technical recession was short-lived in the world of economic data, households and some industries continue to feel the crunch of a slowed economy seen in weak employment growth and low Purchasing Managers' Index (PMI) levels, just to give some examples.

The real estate sector is not immune to economic changes and the climate has been evident in most asset classes, including the office market and the retail sector. Yet the area one would have expected somewhat of a worse shakeup was the industrial sector, which seemingly outperformed the others quarter after quarter. Generally, the sector has maintained low vacancies across both Johannesburg and Durban, two of the most important cities for industrial space. In addition, rental rates reached peak levels in both cities during a year which should have shown increased difficulty. We look at three key trends to watch out for in the industrial real estate sector in 2018.

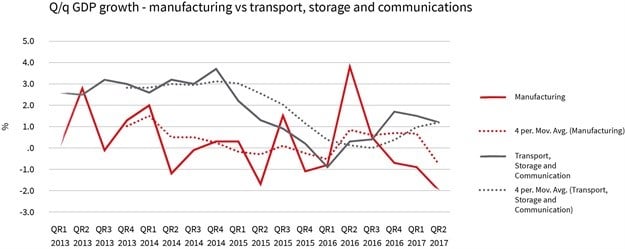

Trend 1: Industrial real estate is becoming less dependent on what happens in manufacturing

The question is if this resilience will continue into 2018 and beyond. As a driver of demand for space in this space, one would have looked at the manufacturing trend and outlook to gain some perspective for industrial property demand. However, it seems that manufacturing as an indicator of industrial real estate demand somewhat weakened during 2017. On a moving average, GDP growth in the transport storage and communications sector has shown a gradual improvement since mid-2016, a divergent trend from the downward contractions recorded in the manufacturing sector.

Data: StatsSA

While the manufacturing sector will always have an effect on industrial accommodation, its significance is expected to be less. Hence PMI values below 50 shouldn’t outright instil fear across the market.

Trend 2: Consumer goods reaching new heights

Consumer confidence remained low for much of 2017, raising concerns for demand in the industrial sector beyond this period. In 2017, we took a close look at Land Transport Survey data (StatsSA) for measurements of land freight activity. It is interesting to note that freight income from consumer goods increased notably. On a year-to-date basis (January- August 2017), freight income from clothing and textiles has increased by 36.0% y/y and freight income from manufactured food by 27.0%. This increase is not just driven by cost-push pressures: PPI inflation averaged around 5% in 2017, while the fuel price, although substantially higher than 2016, has increased by only half of this at 16.0% y/y on a year-to-date basis (January to September 2017).

It is difficult to tell the final destination of goods based on this data alone: freight moves imports goods, exports goods and goods interprovincially. However, it is worth noting that retail sales growth made a recovery going into Q4 2017, reaching 5.5% in August from a 1.7% contraction in January. Caution among consumers is likely to persist and the volatility in retail sales figures is telling of this. As a result, retailers are looking at ways to offer price advantage. One way to do this is to bulk-stock at even larger quantities and negotiate even better prices with struggling manufacturers, leading to higher needs for logistics and warehousing accommodation. A more prudent move is just-in-time stocking, gauging customer demand and reducing order quantities, which could result in lower demand for accommodation. So a close eye on what large retailers are doing should shed some light.

Trend 3: Strategic industrial nodes

Lastly, it is worth considering the impact of the industrial development pipeline and the effect it could have on the sector. In Johannesburg alone, there is at least 500,000m2 of accommodation in the pipeline. The market has also seen growing confidence for the development of non-speculative buildings. Industrial parks have grown in popularity and demand continues to gravitate to modern, high-tech developments, creating tight competition for older stock in the market.

Of particular interest is the gradual establishment of strategic nodes such as Ekurhuleni’s Aerotropolis or eTthekwini’s Dube TradePort. Both located near international airports, these industrial nodes are likely to create real competition in the logistics and warehousing space, albeit in the long term. Both areas offer added appeal for importing and exporting businesses in particular, and any occupier debating a move in a few years’ time could start looking at these areas as an option.

While the industrial market seems far from experiencing an over-supply at current vacancy rates, it is important to note that demand is beginning to flatten. The uncertain consumer market also forewarns of pressure in the market during 2018. Some industrial areas saw a bit of a rental correction in Q3 2017, highlighting that there is some pressure in the market in the year ahead – just not as much as we are seeing in other sectors such as the commercial market.