Q&A with SKIN Functional’s Shannon Dougall

Maroefah Smith

Today, tech savvy car insurance is about developing consumer-centric solutions for the connected mobility era. This presents both a challenge and an opportunity for Africa’s insurance organisations, and they need to wake up and play their part in the global transformation process. Transformation in the industry is fast-paced with major shifts in demographics, economic power, regulation and, more importantly, technology, bringing about a fundamental restructuring of the global insurance industry.

Research on the Internet of Things (IoT) forecasts that by 2020, more than 2.5 billion people will be connected on social networks, there will be 75 billion connected devices and a value of $65 trillion in global business trade. This will ultimately connect people, transform business and reimagine results through new business models and simplified enterprises.

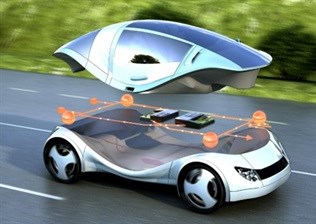

The IoT brings with it a new insurance ecosystem. The future of motor insurance will remain usage-based insurance (UBI), a type of vehicle insurance whereby the costs are dependent upon type of vehicle used, measured against time, distance, behaviour and place. Through advanced offerings, such as SAP’s connected car, insurance brands will be able to adapt and transform quickly and effortlessly with the aid of:

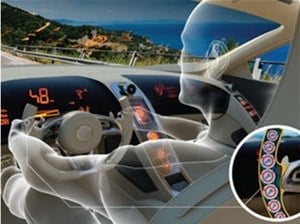

• Telematics, which gathers data that enables auto insurers to receive driving information in real time such as mileage, speed, acceleration, technical vehicle data, location, kilometres driven, time of day, road information, etc. from sensor devices in the vehicle.

• Usage-based insurance, made possible by the telematics information and enabling insurers to offer pay-as-you-drive/pay-how-you drive premiums.

• New business models that allow the insurer to offer additional value added services such as roadside assistance, emergency calls, location-based offers and more to the policy holder to increase customer loyalty and retention by offering rewards.

The need to transform the core operations environment to offer more customised solutions to customers is the critical objective for many - if they are to compete in changing markets and be in a position to counter the threat posed by disruptive new entrants. To date, many insurers have taken steps to become ‘digital insurers’ and although these initiatives are beneficial, they remain isolated from operations and still require significant development and intervention.

The millennial generation, an increasingly important market segment, demand convenience, transparency, flexibility and control when interacting with a brand, especially a brand like an insurer. Yet the industry has traditionally been slow to respond. The connected car is a simple solution that helps to address these business challenges and market requirements.

For example, telematics, one of the latest catchwords in the industry, can be described as the process of long-distance transmission of computer-based information, and has proven to be a powerful and valuable tool to improve efficiency within businesses. When it comes to insurance, it’s apparent that a ‘one-size-fits-all’ approach does not work in terms of pricing. Instead, paying based only on how much the consumer drives is an innovative way to make insurance more affordable.

The usage-based connected car utilises IoT technology to allow insurers to offer accurate premiums and value-added services to individual drivers. The benefits and advantages are vast, and include:

• Assisting insurers to identify, measure and better calculate drivers' risks

• Helping attract low-risk drivers and reduce claims costs

• Offering individual premiums to customers and give them greater control over their premiums

• Increasing the number of potential customer touch-points per year

• Improving customer loyalty and satisfaction

The risk of disruption is real and the pace of change is ever increasing. Insurers need to accelerate their transformation efforts if they are to reduce the risk of being left without a competitive advantage. Software-as-a-service (SaaS) based core operations platforms running on a cloud infrastructure provide a means to move quickly to an integrated channel platform. Insurers have been strong adopters of SaaS and cloud technology – now, the usage-based connected car marks the next evolution.

Motor insurance is changing. Connectivity and auto tech developments are moving the goal posts and insurers need to be more radical in challenging business models. However, challenges do exist; including mounting commoditisation and the need to have lower-cost digital distribution and advanced digital profiling to respond more effectively to customer demands. In order to be successful, insurance companies need to move quickly in developing the necessary competitive capabilities and core business operations. If they’re successful in these efforts, they’ll be able to sustain growth and keep pace with our ever-changing and demanding market expectations.