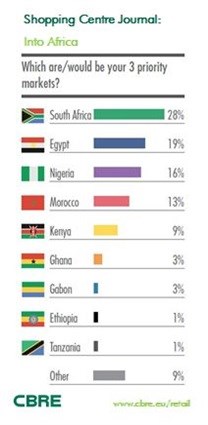

Almost one-third of European retailers view Africa as an important future destination in the next three to five years, real estate advisor, CBRE has advised. In a recent report, CBRE surveyed the expansion plans of 115 leading retailers. Over the next five years, one-third see Africa as extremely or very important retail destination with 28% of respondents viewing South Africa, Egypt (19%) and Nigeria (16%) as key priority markets.

Sixty-four percent of respondents went on to say that franchise stores would be their preferred route to market, and the two areas stopping them from expanding more rapidly into Africa was infrastructure (22%) and easier opportunities elsewhere (21%).

Preston Gaddy, Broll divisional director for strategic retail leasing said: "South Africa remains the preferred starting point for many international brands considering entry into the continent.

"These retailers mostly come from Europe, with a large percentage of retailers from the Middle East that are exploring expansion into cities such as Lagos, Accra, Lusaka and Nairobi, and are not quite ready to take on a South African expansion."

Gaddy explained that whichever region or city on the continent is preferred, the underlying fact is that organic growth in their home markets is somewhat limited. Even though Eastern Europe, Asia and South America is also on their radar, many European and Middle Eastern retailers continue to acknowledge Africa as a key area for expansion, he said.

Number one choice of destination

Andrew Phipps, head of retail research and consulting, EMEA, CBRE said: "South Africa is likely to remain the number one choice of destination due to the presence of the elements retailers want to see: the infrastructure, number of quality shopping malls, and the existing presence of brands being the strong indicators new entrants will look for.

"There is certainly appetite for international retailers to enter the market. The challenge is finding the right partner that understands the market as well as the retail brand."

In terms of infrastructure, there have been significant levels of investment into standby power, way finding and parking as developers contribute heavily towards or upgrade the infrastructure themselves. Investment in existing malls is also taking place with many undergoing major refurbishments and modernisation, he explained.

"GDP growth in sub-Saharan Africa is far higher than in the BRIC countries now, there is a fear that the Chinese stock market is going to decline further and people will look for other avenues for their investments."

"The European market isn't over-saturated, but investors are finding it harder to find what they want and feel there is the option to start to invest in the African market. There is also a belief that investors see a growth in middle-class Africa and don't want to be 'left out'. Population forecasts also sit well as Nigeria is moving towards being the third-most-populous country in the world," according to Phipps.

A slow process

Meanwhile, Gaddy pointed out that entry into new markets may be a slow process and local developers/landlords may not always understand this challenge. It can take anything from two to five years, (in some cases even longer) before the tills start ringing. In most cases this 'circumspect' approach has yielded acceptable results.

He said that some luxury retail brands will have limited opportunities in most major African cities, and in most cases would be limited to four and eight stores per country or region. The economies of scale need to work and critical mass reached to make their entry viable.

Gaddy said that this is where opportunities in licensing, franchising and joint venture arrangements exist. Local retailers, such as the Surtee Group and the Busby Group, have played a key role in the entry by many high-end brands into South Africa.

These companies have, over many years, ensured that brands such as Guess, Aldo, Hugo Boss, La Coste and Armani have been a resounding success. International retailers are seeking more partners of this calibre, as most will not venture into new territories without an experienced local partner.

"We have also seen South African retailers acquiring retail brands, outside of their home markets. The recent acquisition of Office by Truworths and David Jones (Australia) by Woolworths SA are examples of this.

"Equally, other SA retailers, such as The Foschini Group, Mr Price and Pepkor, are all active in the continent. It be could be that perhaps South African retailers are also experiencing the same challenge of limited growth in their home markets, as experienced by their European counterparts," he added.