Q&A with SKIN Functional’s Shannon Dougall

Maroefah Smith

Grant Thornton's tracker data for the second quarter of the assurance and advisory firm's International Business Report (IBR) in 2012 continues to emphasise that poor government service delivery, especially utilities such as electricity concerns, is a real and continuous impediment to business growth in South Africa.

In light of this, Deepak Nagar, Grant Thornton South Africa's national chairman, urges businesses to work together and with Government, to resolve service delivery concerns.

"Corporations have an obligation to meet shareholder objectives and stimulate economic growth. If they are unable to do this, the domino effect is insufficient employment opportunities which ultimately results in an increase in crime," he says. "Only by addressing poor performance on service delivery concerns such as utilities, billing issues and road concerns directly with government, can business help to achieve the country's goals to eliminate poverty and create and reduce inequality."

The Grant Thornton International Business Report (IBR) provides quarterly tracker insights into the views and expectations of over 12 000 businesses surveyed in total per year across 40 economies. The Q2 data for IBR 2012 also highlights regional and national business owner perceptions regarding crime, service delivery and political climate for SA business owners.

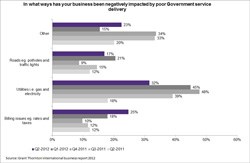

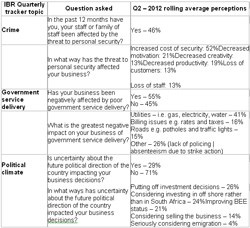

Second quarter IBR data for 2012 reveals that a startling 59% of all SA business owners surveyed are negatively affected by poor government service delivery. This figure is up from 53% recorded in the first quarter of 2012. Data by region highlights that businesses in the Eastern Cape are battling the most with this issue with 65% of business executives surveyed confirming that poor government service delivery is a concern (Gauteng - 54%; KZN - 52% and Western Cape - 50%).

When private business owners were asked to specify what has had the greatest negative impact on businesses in terms of poor government service delivery, 32% stated that utilities (electricity and water) were negatively impacting businesses while 25% stated that billing issues (e.g. rates and taxes) were affecting operations.

"It is interesting to note that sentiment surrounding poor service delivery of utilities has improved by 16% since Q4 2011, from 48% to 32%," adds Nagar, "On the contrary, issues relating to billing concerns is increasing dramatically from 10% in Q4 2011 to the 25% of responses recorded in this second quarter of 2012."

Other items highlighted in relation to poor service delivery issues in Government include roads (potholes and traffic lights), lack of policing (linked to a high crime rate) and absenteeism due to public sector strike action.

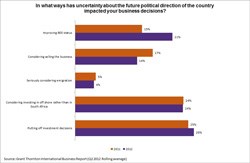

Another macro-economic factor currently impacting SA privately held businesses is the issue of political uncertainly. Grant Thornton's Q2 tracker data for 2012 reveals that sentiment is improving marginally in this regard, with 29% of respondents indicating that uncertainty about the political direction of the country is impacting business decisions (down from 32% in 2011 - rolling average).

Of the 29% affected by political uncertainly, 26% are putting off investment decisions and 24% are considering investing offshore rather than in SA.

"On a positive note, we see that 21% of businesses have made a conscious decision to take action against the political uncertainty currently being experienced in SA, by improving their organisations' BEE status," says Nagar (2011 rolling average:15%). "This is probably in the hope of securing new business contracts by presenting improved empowerment credentials to prospective clientele."

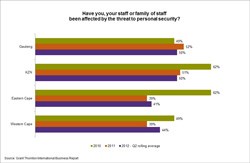

Every quarter, business owners are asked whether they or their immediate family or staff have been directly affected by a threat to personal security (housebreaking, violent crime, road rage, hijacking). Grant Thornton's IBR tracker for the second quarter of 2012 reveals that 46% of privately held businesses have been negatively affected by crime over the past 12 months (2011 rolling average: 46%).

This figure has dramatically reduced by nearly 40%, down from a reported 86% in 2007 when Grant Thornton first began to research this concern. However, the survey highlights an increase of 7%, with 42% of business owners having been affected by crime in Q1 2012, compared to 49% of business owners in Q2 2012. "We cannot accept such a high incidence of crime on our people," warned Nagar. "We need to do everything we can to eliminate this threat once and for all."

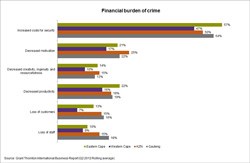

Crime also brings an additional financial burden to privately held businesses. When executives were asked in what ways had a threat to personal security affected business operations 52% stated increased costs of security as the biggest burden, with decreased motivation (21%) and decreased productivity (19%) also highly ranked.

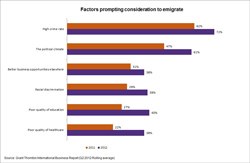

The impact of crime is linked directly to emigration in Grant Thornton's IBR survey with 72% of executives surveyed during Q2 of 2012 stating that the high crime rate is the number one factor prompting them to consider leaving South Africa (2011 rolling average: 62%) Other factors prompting business owners to consider emigrating include the political climate (61%) and poor quality of education (40%).

Reviewing the Q2 2012 data regionally reveals that business owners in Gauteng are most likely to emigrate (25%), followed by executives in KZN (22%) and Eastern Cape (20%), with Western Cape privately held business owners least likely to consider emigrating (10%).

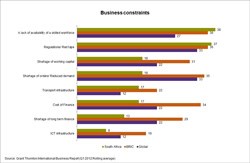

When business owners were asked what they see as the biggest constraint to business expansion, a lack of availability of a skilled workforce (38%) and overregulation and red tape (37%) are by far the biggest factors impeding growth for SA businesses. Countries in the BRIC region concur with both of these factors ranked at 36% by BRIC business owners.

"It seems, however, that organisations in the BRIC economies have a wider range of constraints which are seriously affecting business expansion," adds Nagar. "Factors such as a shortage of orders / reduced demand (35%) and the crippling cost of finance (34%) are also highly ranked as constraints to growth. No doubt the global recession is continuing to dampen these economies."

Global perceptions from over 12 000 business owners in 40 economies are also tracked quarterly.

Business owners are asked each quarter to state how optimistic or pessimistic they are about their country's economic for the next 12 months. The Q2 rolling average economic data relating to Grant Thornton International's Optimism / Pessimism Index, shows that South Africa's optimism balance for the second quarter of 2012 is +53% compared to +58% in 2011 and +60% recorded for the same period in 2010. This is against a global optimism balance of just +12% (2011: +16%) and BRIC optimism of +35% (2011: +40%).

An "optimism balance" is the proportion of business owners reporting they are optimistic less those executives reporting they are pessimistic.

South Africa ranks 7th in terms of global optimism, behind Peru (96%), Chile (90%), Philippines (90%), Georgia (83%), Canada (70%) and India (67%).

"Optimism is down worldwide compared to the first quarter of 2012 and also in comparison to prior years. It is clear that the economic crisis is still far from over," says Nagar. "But business owners in South Africa and in the BRIC economies seem, on the whole, to be a lot more optimistic about the economic conditions for the year ahead, when compared to the global average."

The Grant Thornton International Business Report (IBR) provides insight into the views and expectations of over 12 000 businesses per year across 40 economies. This unique survey draws upon 20 years of trend data for most European participants and 10 years for many non-European economies.

Data collection is managed by Grant Thornton International's core research partner -Experian. Questionnaires are translated into local languages with each participating country having the option to ask a small number of country specific questions in addition to the core questionnaire. Fieldwork is undertaken on a quarterly basis. The research is carried out primarily by telephone.

IBR is a survey of both listed and privately held businesses. The data for this release are drawn from interviews with 3000 businesses from all industry sectors across the globe conducted in May/June 2012. The target respondents are chief executive officers, managing directors, chairmen or other senior executives.