Even if you haven't read this particular Taleb paper, you may have heard comments such as:

These are just a few of the statements that reveal how little many of us know about volatility. Since the FTSE/JSE All Share Index hit an all-time high on 29 July this year, we've witnessed the return of index ups and downs - locally and internationally. Already investors are becoming jittery and checking with their advisers whether it's time to get out of the market.

Maybe now is a good time to debunk some of the myths surrounding market volatility.

Sometimes we forget that volatility is simply the extent to which an investment's monthly returns deviate from their average on a month-by-month basis. The most common measure of volatility is the standard deviation, which, in the case of unit trusts, can be found on the fund's fact sheet. In the table below, Fund A has quite dramatic swings between stellar and pedestrian monthly returns, but no negative months. It therefore has a higher volatility (1.8) than Fund B (0.8), which has poor but consistent monthly returns.

| Jan | Feb | Mar | Apr | May | Jun | Jul | Aug | Sept | Oct | Nov | Dec | Std dev | |

| Fund A | 4.1 | 2.1 | 5.2 | 1.0 | 3.9 | 0.5 | 4.4 | 0.2 | 3.8 | 0.9 | 2.2 | 0.1 | 1.8 |

| Fund B | 0.9 | -0.1 | 1.1 | 0.1 | 0.5 | -0.4 | 1.9 | -0.2 | 0.8 | -0.8 | 1.0 | -0.4 | 0.8 |

As the example above illustrates, high volatility does not necessarily mean an index or a fund's returns have been negative often (although this could very well be the case). It means the returns fluctuate in a wider range than is the case for an investment with a lower volatility. When interested in an investment's negative returns, it's therefore more useful to request a table with all the monthly returns and check the quantity and the extent of the draw-downs than looking at volatility measures.

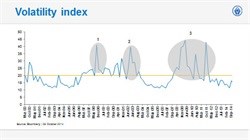

It is quite common for investors to believe that increased volatility is a precursor to a bear market. But there is little evidence of a causal relationship. The VIX or 'fear index' is the most commonly used indicator of the level of volatility that global markets are expecting over the next 30-day period (looking forward), and has a high correlation with the historical standard deviation of the markets (looking back). When the VIX spikes, it's a sign that the market is expecting returns to either shoot upwards or downwards - not only downwards.

Over the past 15 years, there were three periods during which the VIX exceeded 35 (around 20 is the average): August 1998, September 2002 and March 2009.

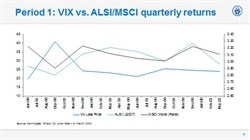

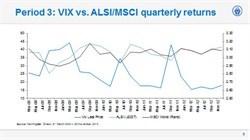

To investigate whether higher volatility introduces a bear market, we've plotted the VIX index against the monthly and quarterly returns of the FTSE/JSE All Share Index and the MSCI World Index for the three periods following the VIX peaks. In the graphs below, the left axis shows the level of the VIX, while the right axis shows the monthly and quarterly returns respectively.

Yes, there were some negative monthly returns after each volatility spike, but one or two months hardly count as a bear market. In contrast, if you look at the quarterly returns after each spike in the VIX index, there are no draw-downs.

Therefore, although we refer to the VIX as the 'fear index', there is no evidence that a rise in the VIX necessarily introduces a bear market. It doesn't mean that a rise in volatility cannot lead to a bear market, though.

Despite the fact that there's no evidence that a rise in volatility leads to a bear market, there are investors who take their money out of the equity market soon after experiencing one or two sharp negative months. By sitting on the side, they run the risk of missing out on some of the best returns of the decade. The bar chart below shows the impact in case you missed the best 10, 20 and 30 days of the last ten years. And the longer you stay out of the market, the greater risk you run of sacrificing returns because of your fear of a bear market (which may never materialise).

Source: Morningstar Direct - ten years to 31 August 2014 and SI calculations

Yes and no. It depends on the angle from which you view volatility. Volatility is important to long-term investors because they need to invest in riskier, more volatile assets to beat inflation over time. Volatility is therefore one of the tools that they use to outperform the conservative portfolios aimed at short-term investors. So, yes, volatility as a tool to unlock long-term value matters.

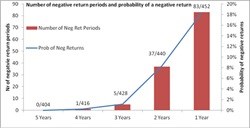

However, the fear or avoidance of volatility should only matter to short-term investors. Long-term investors have time on their side to sit out the ups and downs of the equity market. In the graph below we show how unscathed long-term investors are by negative short-term returns.

Over a number of periods measured from 1976 to August 2014, the probability of capital loss (measured as the number of negative return periods divided by the total number of measured periods) decreases to zero over a five-year period. This indicates that, provided investors are willing to remain invested in the ALSI for at least five years, there is little likelihood of capital loss over the full investment term.

Source: Inet Bridge, Morningstar Direct 1976 to August 2014 and SI calculation

To conclude, volatility is the friend of the long-term investor. By staying the course and ignoring the 'noise' of short-term market fluctuations, and remaining invested through all market cycles, long-term investors will reap the rewards of patience and persistence.